In today’s fast-paced world, understanding finance is essential to building a secure and prosperous future. Whether you’re just starting your career, planning for retirement, or looking to grow your investment portfolio, financial planning is a crucial aspect of long-term success. In this guide, we’ll explore key financial strategies that can help you achieve financial independence, manage your wealth efficiently, and set yourself up for financial success.

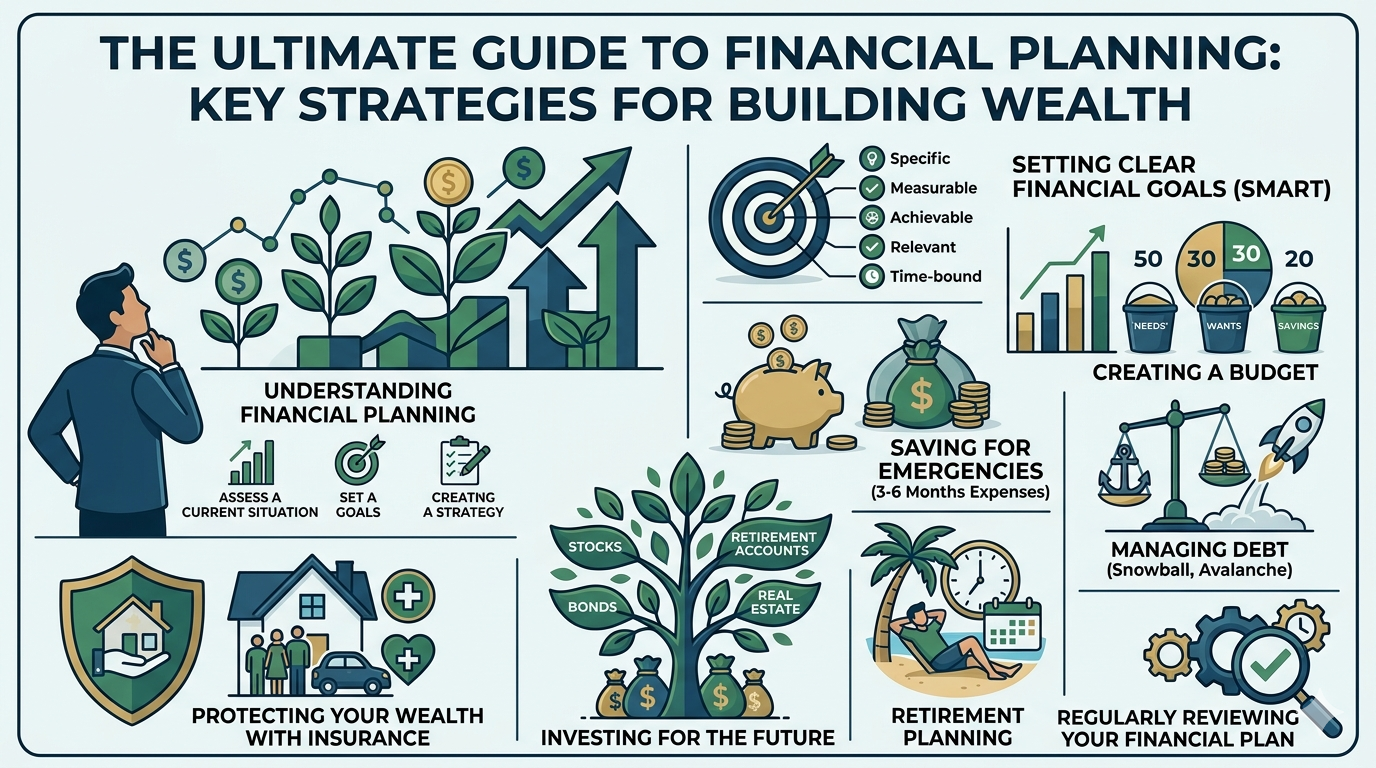

1. Understanding Financial Planning

Financial planning is the process of assessing your current financial situation, setting goals for the future, and creating a strategy to achieve those goals. It involves budgeting, saving, investing, and planning for unexpected financial challenges. The primary objective of financial planning is to ensure that your financial resources are being used effectively to support your long-term aspirations.

A well-organized financial plan can help you stay on track, avoid financial stress, and make better decisions when it comes to handling your finances.

2. Setting Clear Financial Goals

One of the first steps in financial planning is setting clear and measurable financial goals. These goals can be short-term (like paying off debt or saving for an emergency fund) or long-term (such as buying a home, funding your children’s education, or saving for retirement).

When setting goals, it’s important to make them SMART: Specific, Measurable, Achievable, Relevant, and Time-bound. For example, instead of saying, “I want to save more money,” a SMART goal would be, “I will save $500 each month in my emergency fund for the next 12 months.”

3. Creating a Budget

A budget is the foundation of any financial plan. It allows you to track your income, expenses, and savings so you can ensure that you’re living within your means. Creating a budget can help you avoid unnecessary debt, build an emergency fund, and allocate funds towards your goals.

There are several popular budgeting methods you can use, including:

- 50/30/20 Rule: Allocate 50% of your income to needs (housing, utilities, etc.), 30% to wants (entertainment, dining out), and 20% to savings and debt repayment.

- Zero-Based Budgeting: Allocate every dollar of your income to a specific expense or saving goal, so that you end up with zero at the end of the month.

4. Saving for Emergencies

Building an emergency fund is one of the most important financial steps you can take. Having money set aside for unexpected expenses like medical bills, car repairs, or job loss can prevent you from going into debt during tough times.

Experts recommend saving three to six months’ worth of living expenses in an easily accessible savings account. Start small, but remain consistent. Even setting aside $100 each month can add up over time.

5. Managing Debt

Debt can be a significant barrier to financial freedom. High-interest debt, such as credit card debt, can quickly accumulate and make it harder to save and invest. Managing and reducing your debt should be a priority in your financial plan.

Some effective strategies for managing debt include:

- Debt Snowball Method: Pay off your smallest debts first, then move on to larger ones. This method helps build momentum and motivation.

- Debt Avalanche Method: Focus on paying off high-interest debts first, which will save you money in interest over time.

- Consolidating Debt: Consider consolidating multiple debts into one loan with a lower interest rate to make your payments more manageable.

6. Investing for the Future

Investing is one of the most powerful ways to grow your wealth over time. The earlier you start investing, the more time your money has to compound and grow. There are many different types of investments, including stocks, bonds, real estate, and retirement accounts.

- Stocks: Investing in individual stocks allows you to buy shares of companies. Stocks offer higher potential returns but come with higher risk.

- Bonds: Bonds are loans to governments or corporations that pay interest over time. They are generally considered safer than stocks but offer lower returns.

- Retirement Accounts: Contributing to retirement accounts like 401(k)s or IRAs offers tax advantages and helps you build a nest egg for your later years.

- Real Estate: Real estate investing can provide passive income and appreciate in value over time, but it requires a higher initial investment.

Before you begin investing, it’s important to assess your risk tolerance and time horizon. If you’re unsure about how to start, consider consulting with a financial advisor.

7. Retirement Planning

No matter your age, it’s never too early to start planning for retirement. The earlier you begin, the more time your investments have to grow. In addition to contributing to employer-sponsored retirement plans like a 401(k), you can also open individual retirement accounts (IRAs) for additional tax benefits.

There are two main types of IRAs:

- Traditional IRA: Contributions are tax-deductible, but you’ll pay taxes on withdrawals in retirement.

- Roth IRA: Contributions are made after-tax, but withdrawals are tax-free in retirement.

The goal is to have enough retirement savings to maintain your standard of living once you stop working. Experts recommend saving at least 15% of your income each year for retirement, but the exact amount will depend on your desired lifestyle and goals.

8. Protecting Your Wealth with Insurance

Insurance is an essential part of financial planning. It provides financial protection in case of unexpected events, such as illness, accidents, or property damage. Key types of insurance to consider include:

- Health Insurance: Helps cover medical costs and protects you from unexpected healthcare expenses.

- Life Insurance: Provides financial support for your dependents in case of your death.

- Disability Insurance: Protects your income if you’re unable to work due to illness or injury.

- Home and Auto Insurance: Protects your property and vehicle against damage or theft.

By having the right insurance in place, you can prevent large, unexpected costs from derailing your financial plan.

9. Regularly Reviewing Your Financial Plan

Financial planning is not a one-time activity. Your financial situation, goals, and priorities will change over time, so it’s important to regularly review and adjust your plan. Set aside time each year to assess your progress, make necessary adjustments, and ensure that your goals remain realistic and achievable.

Conclusion

Effective financial planning is key to achieving financial security and wealth. By setting clear goals, budgeting effectively, saving for emergencies, managing debt, and investing wisely, you can take control of your financial future. The earlier you start planning, the more time your money has to grow and the better prepared you’ll be for any challenges that may arise.

Remember, financial planning is a continuous process, so stay committed to reviewing and refining your strategy to ensure you’re on track to meet your goals. With diligence, discipline, and the right financial strategies, you can secure a prosperous future for yourself and your family.